Outside earnings, do cyber companies ever have good news when the market closes? Not really… Does it make sense to pay a tiny amount of interest every day for shorting a few cyber stocks, and when stuff blows up, you just don’t buy it back when the market opens?

Not financial advice

Why this might work:

- You always have good liquidity, trading in the opening and closing auctions

- You only trade major names, because only major names can cause major damage

- You can hedge well against Nasdaq 100 futures

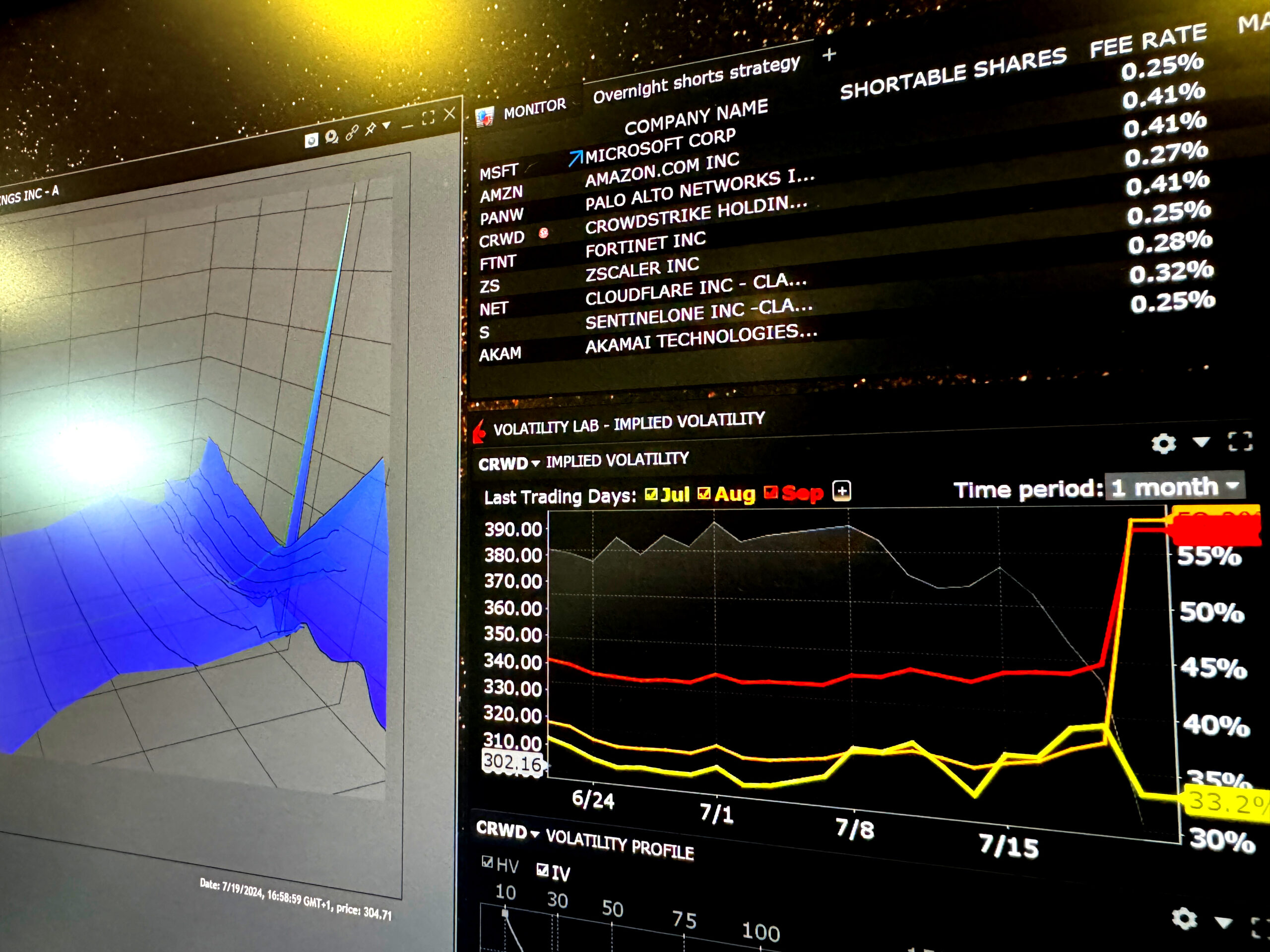

If you shorted CRWD at market close yesterday and bought back at the open, you would have had a 15% return. What would it cost to always hold a few names short, in case one tanks?

Why this might not work:

Fees.

Thesis: only bad stuff happens overnight for IT stocks

- Market data costs are essentially zero (I just need delayed data and a sentiment bot to wake up my phone if bad news happens overnight)

- Volumes are huge so I won’t cause much slippage

- Shortable shares are often plenty so the strategy won’t struggle to borrow

- I can trade in options too, which may have lower transaction costs than shares

- Interest paid will be small, and historically the Nasdaq does well – remember I’m hedged long NDX

- In a massive catastrophic event when I cannot de-risk, I am already short, which is probably useful

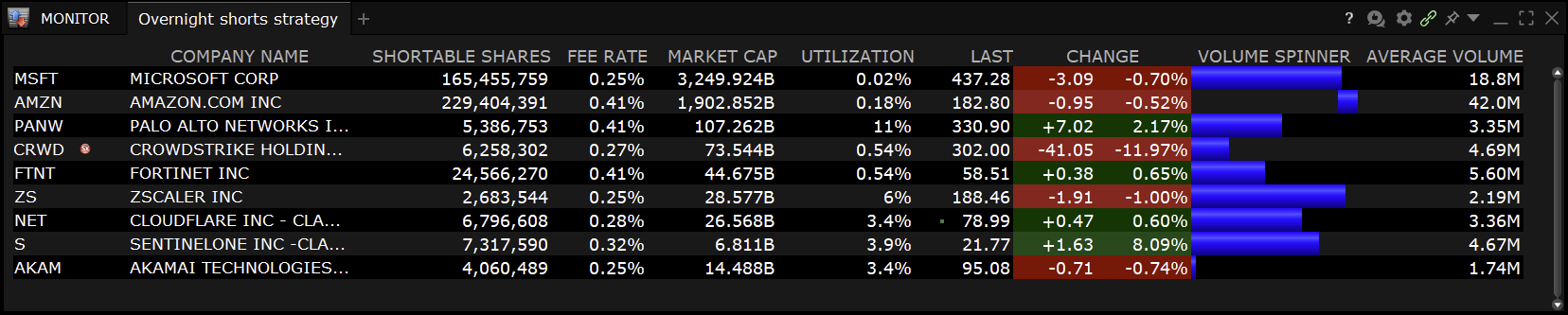

List of stocks often used in critical IT paths

I’m particularly interested in CDNs, hyperscalers and infosec firms – they often cement themselves in critical parts of many businesses as single points of failure. Here’s my list:

Maths and strategy

- On my broker, I see annual borrow fees of about 0.31%

- I take the view I’ll see one major blow up per 2.5 years

- Over the last 5y, the NDX has grown 75% per 2.5 years which pays off my borrow costs easily

- I take profit when I see a 10% after-hours fall (bot buys to cover in the am)

- I close individual positions during earnings – I am not taking views on fundamentals

- We equal weight the names (else we are too heavily skewed toward Microsoft and Amazon, 95% of market cap of my list above)

- Expanding the portfolio doesn’t help. There are very few companies that can badly screw up global tech.

If I expect one blow-up every 2.5 years in my portfolio, taking profit at 10%, I have an annual expected profit of:

[latex] AnnExpProfit = \frac{take\_profit\_percent * leverage}{portfolio\_name\_count * years\_per\_blowup} – borrow\_costs\_per\_blowup[/latex]

Borrow costs per blowup is just an annualized interest rate over 2.5 years.

That’s about 1% per year returns above the NDX before fees.

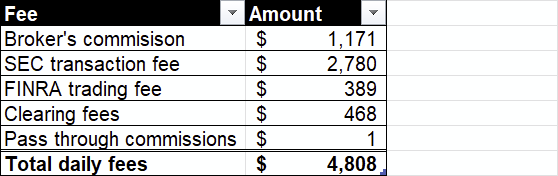

Transaction fees

Oh yeah… suddenly this is way less sexy.

- Broker’s commission: $0.001 * quantity

- SEC transaction fee: $0.0000278 * value

- FINRA trading fee: $0.000166 * quantity

- Clearing fees (NSCC and DTC): $0.0002 * quantity

- Pass through commissions: 0.00735 * broker’s commission

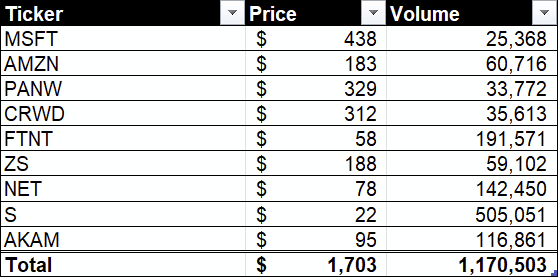

If we’re running $100MM on this strategy (say $25MM x4 leveraged) and trading half of that in stocks (the other half is the hedge), that’s about $50MM every time we go in or out, so $100MM per day. Quantity-wise, that’s 1.4 million shares per day. We trade twice a day so average daily voumes are 2.8 million.

There’s no way this will work. With 252 trading days in a year, minus one for earnings, that’s $1.3MM in fees per year. On a $100MM book making 1.3% above the benchmark per year gross, that’s a 0.3% loss per year.

This strategy is expected to lose money. We won’t trade it via cash equities.

Beta risk and investment horizons

I am mostly beta-neutral. I’d probably go slightly more long NDX than short my overnight names because I have a 2.5 year investment horizon. I want to see my capital make money passively when there is no drama.

What about using options?

I’m not convinced. Close to expiry (but not 0DTE) options might be an… option, traded OTM (because we want large moves). A curious look shows $0.20 spreads and I’ll pay $0.15/contract with my broker. Then come all the usual fees as well, including the SEC and FINRA transaction fees, an ORF (Options Regulatory Fee) of about $0.02/contract and more clearing fees that could be as high as $55 per trade, twice a day.

Without calculating, the SEC and FINRA fees alone are still about 60% of the $1.3MM in fees from equities.

Trading with options will probably lose money too, due to fees.

Could we reduce TCs by being permanently short?

This would be a large trading cost saving but would alter the risk profile, as we now are exposed to intraday news. We would be taking the view:

“The Nasdaq will outperform IT stocks, including MSFT and AMZN”

…which is quite a view, especially with heavily crowded AI trades. OpenAI and AWS have been huge recent drivers of US equities growth, so this is a bold view to say they’ll underperform the rest of the Nasdaq.

I would estimate we might rebalance once a month, so I’m now trading 24 times a year, so TCs are now $123k pa, but the risk profile is pretty dangerous now.

Let’s quantify it. On Yahoo! Finance I grabbed 5y OHLCV data (I only care about Adj Close), and I load this into Pandas. I did this for all 9 portfolio names, as well as ^NDX.

Using numpy, pandas and scipy I load in all files in my directory that are CSVs. I have a special handling case for ^NDX. I have data frames for stock_data and nasdaq_data now.

I then proceed to read these in and calculate VaR and expected portfolio volatility:

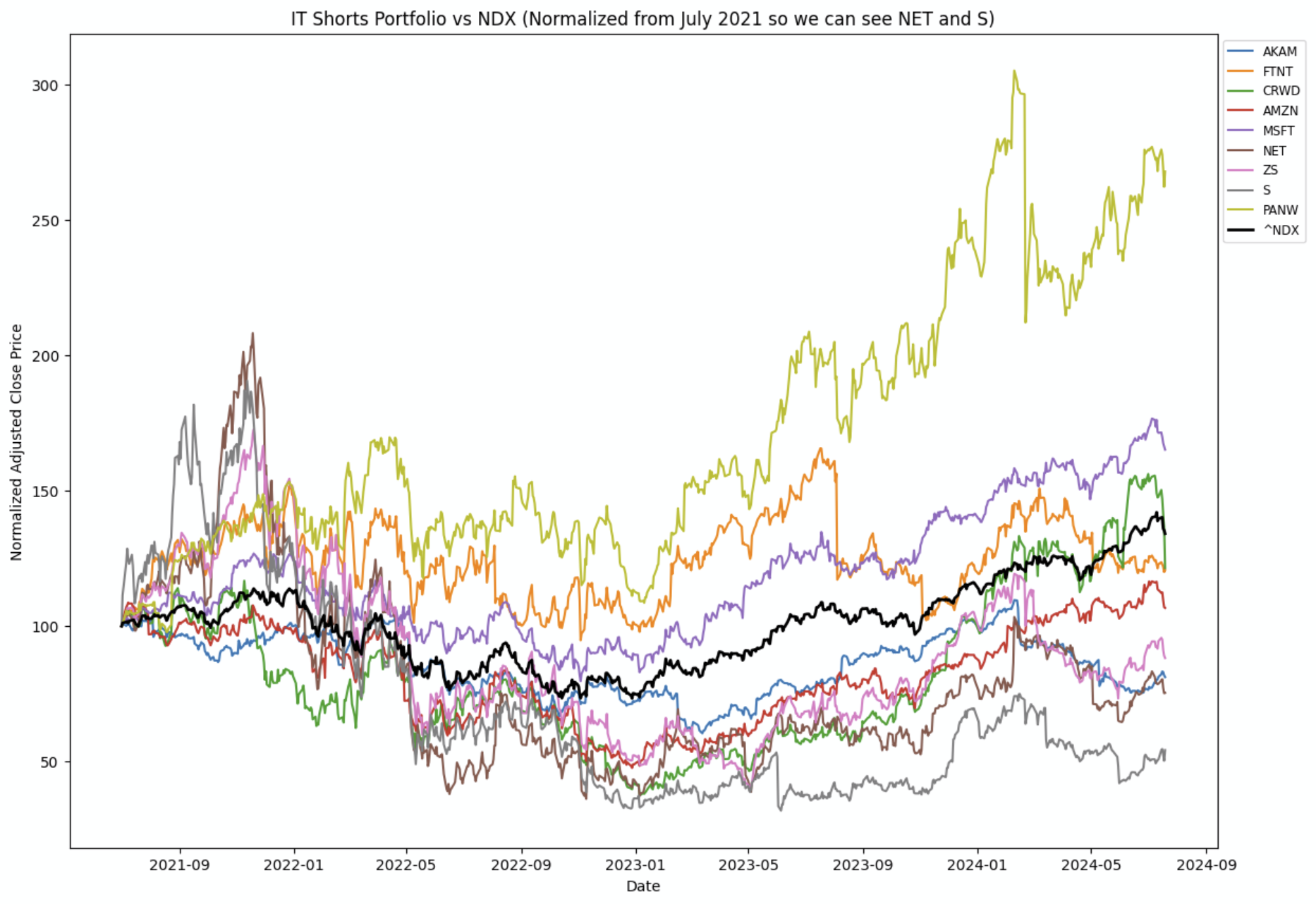

For visualization’s sake, here’s normalized returns of the portfolio versus the index:

Staying permanently short is too risky: there’s a 5% chance I lose about 19% of my leveraged amount in a day – I’d get stopped out and fired by the CIO.

What’s the hedge?

As mentioned, buy NDX futures overnight to the same dollar value as our overnight short positions.

Regulatory blockers?

- SEC Rule 201 (uptick rule) won’t be a problem because we are already short before the 10% drop that triggers the rule.

Should we trade telcos?

Nope, BGP is a great protocol used in the Internet; it would be so difficult for a single name stock to take down the global Internet.

Why is Google missing on your list?

Because Google Cloud Platform is not in critical paths to the same extent a firewall firm is, or a CDN.